The Minimum Payment Lie

The statement arrives. You open it.

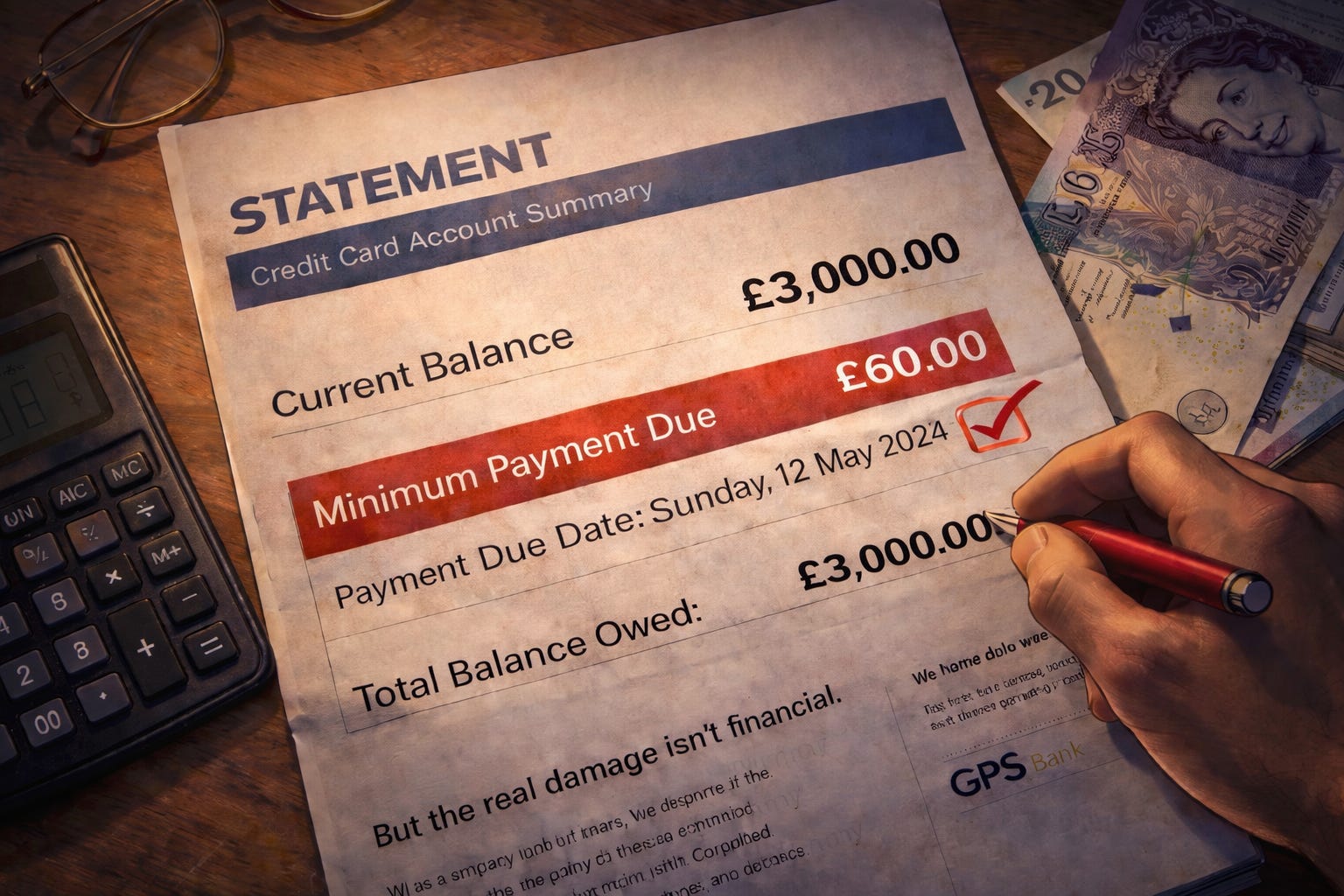

The number at the top is uncomfortable, bigger than you’d like, a reminder of a month that got away from you. But then your eyes drop lower, to the smaller number. The friendlier one. The one that says minimum payment due.

And something in you relaxes.

You pay it. You feel responsible. You move on.

That feeling, that quiet exhale of relief is the most expensive emotion in personal finance.

Here is what actually happened in that moment.

You didn’t manage your debt. You rented it for another month.

The bank took your payment, covered the interest it was owed first, applied a few pounds to the actual balance, and reset the clock. Next month, interest will accrue again on almost the same amount. You’ll get another statement. You’ll feel that same relief. And the cycle will continue, not for months, but potentially for years.

This isn’t an accident. It is a design.

The minimum payment wasn’t created to help you get out of debt.

It was created to keep you in it, comfortably enough that you don’t panic, just long enough that the bank makes far more from you than you ever intended to give.

Think about the language for a second. Minimum payment due. Not the amount that will cost you the least. Not what you should pay. Just the minimum. The floor. The bare threshold that keeps you from being flagged as a problem.

And by putting that number on the statement, small, neat, unthreatening, the bank does something clever. It becomes the number your brain anchors to. Not the total balance. Not what you actually owe. Just the minimum. Everything above it feels like a bonus. Like you’re doing extra.

You’re not doing extra. You’re barely treading water.

Here’s the reality nobody runs the numbers on.

A £3,000 credit card balance at a typical UK interest rate, paid on minimum payments only, doesn’t take a year to clear. It doesn’t take two. It takes the better part of a decade and by the time it’s done, you’ll have paid close to double what you originally spent. The purchases are long gone. The interest lives on.

That jacket. That weekend away. That series of small things you don’t fully remember. You’re still paying for them. Years later. With money you could have used for something that actually mattered.

This is what the minimum payment does. It converts short-term spending into long-term debt, quietly, automatically, month after month, while you feel like you’re handling it.

But the real damage isn’t financial. It’s psychological.

When you pay the minimum, you feel like you’ve done something. The account is in good standing. No late fee. No angry letter. No problem, not today, anyway.

And that feeling of no problem today is what makes the trap so effective. Because the problem isn’t today. The problem is accumulating silently in the background, growing a little every month, while your attention is elsewhere.

This is how debt stops feeling urgent. Not because it’s gone but because the discomfort has been perfectly managed. Spread thin enough that you never feel it sharply enough to act.

The bank doesn’t need you to be in crisis. It just needs you to be comfortable enough to stay.

There’s a version of this that’s even quieter.

You’re not struggling. You earn reasonably well. The minimum payment isn’t even a stretch, it’s just convenient. You pay it because paying the full balance feels unnecessary when the minimum keeps everything ticking over.

This is the version that catches people off guard the most. Not the person who is genuinely cash-strapped, but the person who simply never stopped to question whether the minimum was ever meant to work in their favour.

It wasn’t.

The minimum payment is the bank’s preference. Not yours.

So what does clear thinking actually look like here?

Not stress. Not guilt. Just one shift in how you see the statement.

Stop looking at the minimum payment as the number to pay. Start looking at the total balance as the number to shrink. Even an extra £30 or £50 above the minimum each month compresses years of repayment into months. The interest you don’t pay is money that stays with you, for something you actually chose, rather than something you’re still paying off from two years ago.

The goal isn’t perfection. It’s not clearing the balance in one go. It’s simply refusing to let the bank set the terms of your repayment on your behalf.

Because the moment you accept the minimum as the plan, even temporarily, you’ve handed control of your timeline to someone whose interests are not yours.

The minimum payment keeps you legal. It doesn’t keep you free.

That’s the lie at the centre of it. Not that the number is hidden, it’s right there on the statement. But that paying it feels like progress when really it’s just permission for the debt to stay a little longer.

And debt that stays a little longer always ends up staying a lot longer.

This is Issue 2 of Clear Money Thinking, part of a series on debt, EMIs, and the modern money traps hiding in plain sight.

Next week we’re going deeper into something that’s quietly become a middle-class identity: EMI culture, and why the generation that earns the most is somehow always broke.

If you’ve been forwarding these to people, thank you. That’s how this grows.

And if someone sent this to you, welcome. This is what we do here. One clear idea a week, no noise.

Subscribe below. It’s free.

— Chetan

Reply to this. I read everything.

Clear Money Thinking - Calm thinking in a loud money world.

New essays every week. Free to subscribe.